Christian economics

How can we apply Christian teaching to make the economy work for everyone?

What is Christian economics?

Christian economics is a difficult concept to wrap our heads around, partly because economics is relatively new. While some concepts go back to the Middle Ages, such as in the work of Thomas Aquinas, 18th century English philosopher Adam Smith is credited with establishing the science as we know it. The Bible has numerous teachings on economic issues, such as the Old Testament law for merchants to use honest weights and measures and the one prohibiting usury (excessive interest); but the spiritual mind does not easily meld with the scientific one.

This is not to say that no one has tried. There is a society of professional economists, the Association of Christian Economists, that publishes a peer-reviewed quarterly journal with articles treating economics from a Christian perspective.

I am not an expert in this subject, but am offering here an introduction by offering twelve principles that should guide Christians in their economic lives. In the second part of this post, I shall offer some thoughts on how we can as a society preserve free enterprise while broadening the access of all to economic opportunity by closing the wealth gap.

Twelve Principles of Christian Economics

In 2019, Dr. R. Albert Mohler, Jr., presented to the Christian Business Men’s Connection in their Executive Forums space a list of twelve principles that should guide a Biblical worldview on economics. Here is a simplified list:

1. God’s glory. Economic systems should reflect God’s character and purposes. (I Corinthians 10:31)

2. Human dignity. Because every individual is made in God’s image (Genesis 1:27), every individual should be treated fairly in economic transactions.

3. Private property. The Eighth and Tenth Commandments against stealing and coveting, support the right to private property. All of us have the right to own and manage personal resources. (Exodus 20:15,17)

4. Stewardship of resources. When God gave humanity dominion over the earth, he made us responsible for managing its resources wisely. (Genesis 1:28)

5. Generosity. Reflecting God’s generosity toward us, we must be generous to the poor and needy. (Proverbs 11:25)

6. Work ethic. God calls us to work diligently. (Colossians 3:23). The ancient Nation of Israel prospered as the result of hard work and productivity.

7. Justice and fairness. Economic systems should ensure that economic systems give all individuals access to economic opportunities. (Proverbs 21:15)

8. Community and cooperation. We should all work together for the common good. (Acts 2:44-45)

9. Avoiding debt. The Bible warns against excessive debt (Proverbs 22:7). We are expected to live within our means and to be responsible with our finances.

10. Wealth is a tool, not an end. Wealth is to be used for God’s purposes, not hoarded. (Matthew 6:19-21)

11. Accountability. We will be held accountable for the way we manage our resources. Again, we are called to be responsible stewards of what God has entrusted to us. (Matthew 25:14-30)

12. Hope and Future. In making financial decisions, we should be forward-looking in planning and decision making, reflecting hope and a future grounded in God’s promises. (Jeremiah 29:11)

Even with these principles, economics is a vast subject. Certainly, these principles can and often do influence business owners in their employee and customer relationships; but how do we look at them from a macro perspective? 1 There is one issue that encompasses most of the economic ills we face in our society – wealth inequality.

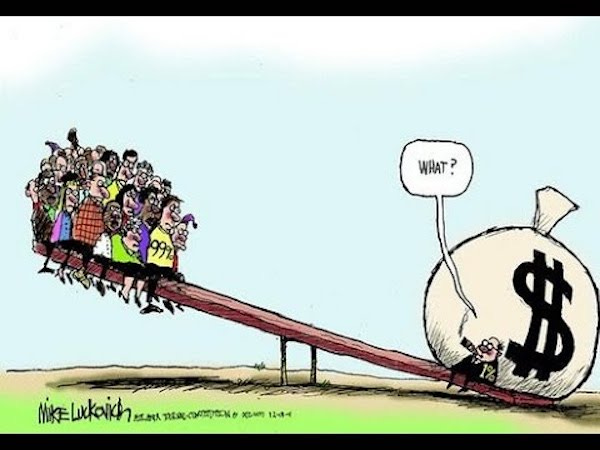

Wealth inequality

We have seen the statistics (Federal Reserve Bank data): Fifteen years ago (3rd quarter 2010), the top 1% of Americans owned 28.4% of the nation’s wealth, while the bottom 50% held only 0.5%. In the 3rd quarter of 2025, the top 1% held 31.7%, while the bottom 50% held 2.5%.

We also have the highest wealth inequality of any advanced industrial democracy. The World Bank measures wealth inequality using the Gini coefficient, where a score of 0 represents perfect equality of wealth among all people, and 100 represents one person holding all the wealth. Thus a lower score is more desirable. The score for the United States is 41.8, while most European and other advanced countries score in the twenties and thirties. (The highest wealth inequality is in South Africa – 63.0, with many African and South American countries scoring in the fifties. Our nearest neighbor, Canada, scores 29.9).

An obvious solution is to greatly increase governmental intervention in the economy under a set of policies loosely grouped under the heading democratic socialism. However, experience shows that high governmental regulation will tend to follow the political Golden Rule: He who has the gold gets to make the rules.

I asked Microsoft Copilot this question: How can we reduce wealth inequality consistent with free enterprise? I have struggled with this for years – but AI could deal with it in about two minutes – with surprisingly reasonable results. I have edited those results into a series of general policy suggestions:

1. Make markets more competitive, not more rigged. Strengthen antitrust enforcement so that upstart firms can compete against the established ones, and simplify government regulations (such as licensing rules, zoning laws, and complex compliance regimes) to lower barriers for entrepreneurs to move, start businesses, and grow wealth. We need a competitive market, not winner-take-all.

2. Change taxation rules to broaden asset ownership. Develop policies that encourage lower- and middle-income households to own stocks, retirement accounts, and business equity, without capping the upside for the rich. Furnish “baby bonds” and starter asset accounts to help children, especially from low-wealth families, to give them a stake in capital markets, while those markets would still determine returns. Encourage employee ownership and profit-sharing. In short, enable more people to hold capital.

3. Design taxes to be more market-friendly. Earned income tax credits preserve take-home pay for workers while preserving incentives to work and hire. A flat tax ensures that everyone pays their fair share, while keeping strong incentives for innovation and investment. We can reduce poverty by setting a floor below which no tax is collected. We thus encourage a redistribution of wealth without interfering with the operation of markets.

4. Remove structural barriers to mobility, by reforming zoning laws that inflate property values out of reach of most home buyers, and enable families to move to where jobs and good schools are. Comprehensive public transit systems will also increase mobility. Over time, we can reduce inequality by ensuring that all children have access to high-quality education and skills training. Finally, ensure that benefits travel with the worker (not the employer), so that workers can freely change jobs, start businesses, or move. We are not trying to flatten outcomes, we are flattening obstacles.

5. Encourage entrepreneurship from the bottom up. Create new tools to enable small and minority-owned businesses to get credit on fairer terms. Reduce the cost and paperwork required to start a new business, and provide incubators to help those in underserved communities translate ideas into viable enterprises. In the words of my source, “capitalism should be a ladder, not a scoreboard.”

6. Curb extreme concentration, not ambition. Strengthen shareholder rights and ensure that shareholders can get full disclosure of corporate activities in a simple, readable form – so that excessive wealth does not flow to top management.

7. Change campaign finance and lobbying rules to reduce the ability of concentrated wealth to shape rules in its favor.

We don’t want to punish success, we just want to prevent the successful from writing the rules to lock the rest of us out.

Links suggested by Copilot (which I have not reviewed):

Six policies to reduce economic inequality | Othering & Belonging Institute

https://belonging.berkeley.edu/six-policies-reduce-economic-inequality

Government policies to reduce income inequality | OpenStax

Free Markets and Capitalism Can Reduce Income Inequality | National Review

https://www.nationalreview.com/2025/03/democratizing-american-prosperity/

Conclusion

We don’t want to punish success, we just want to prevent the successful from writing the rules to lock the rest of us out.

These changes do not necessarily have to expand the size or scope of government (which I oppose in principle as a Libertarian). Many of the above suggestions will reduce bureaucracy, and several of them do not require government participation at all. Reducing income inequality will take creativity and some grit – but then the Gospels never said it would be easy.

Faithful Citizen with Harold Thomas consists of the musings of a mainline Protestant, libertarian Boomer who tries to keep up with the news while remaining true to his faith and the principles of the American Founders. Harold is an author and retired business analyst with degrees in political science and foreign service living in Columbus, Ohio.

What are your thoughts? Share your comments with us. Likes and restacks are also greatly appreciated!

The study of economics is divided into microeconomics, the science of running a business; and macroeconomics, which deals with governmental fiscal and monetary policy.

I hope I am known as “faithful” someday. That’s what I want to be known for. Gaming dad here working on a new book titled Christian Gaming Dad. I’m posting each chapter on my Substack for free.